Ah, customization.

The quintessential aspect of great consulting work.

In my view, the main reason why top consultants are so highly paid and respected is that they can adapt academic business theory (that seems to only work in theory) to the specifics of each client and their situation.

Being structured, hypothesis-driven and everything else related to consulting is merely a means to that.

Management consultants, in essence, bridge the gap between theory and practice.

They deeply understand their client’s situations and are able to understand which piece of “theory” fits their situation. They’re also able to mix and match different theoretical frameworks to solve unique problems, and often times they even come up with theory on their own.

What does this has to do with creating customized profitability trees, you ask?

Everything!

As we saw on the supermarket examples above, having a customized structure to solve your problem lets you see it in a more intuitive way.

It also helps you see what the problem may be a more precise way.

And what we did to build it was to essentially build the gap between theory (the archetypical profitability framework) and the practice (how a supermarket really works and the metrics that matter for them).

And in fact, we could’ve done an even better job. Here’s how I’d build an even better profitability tree for the supermarket industry:

(I’ll teach you how to build it in this very section!)

This Profitability Tree is fully customized for the supermarket industry.

It wouldn’t be as good for any other type of business (although it could work well for some other types of retailers).

It’s still not perfect, though – no issue tree is perfect (and perfect should never be your goal).

For example, I didn’t include credit card processing fees in there.

Had I included it and all possible costs of a supermarket, the tree wouldn’t be perfect either as it would be too extensive and not 80/20.

When building any kind of issue trees, including profitability trees, you’re always aiming for very good, not perfect.

Still, it helps to know what makes this profit tree very good before we jump into how to build trees like these.

Here are the three main reasons:

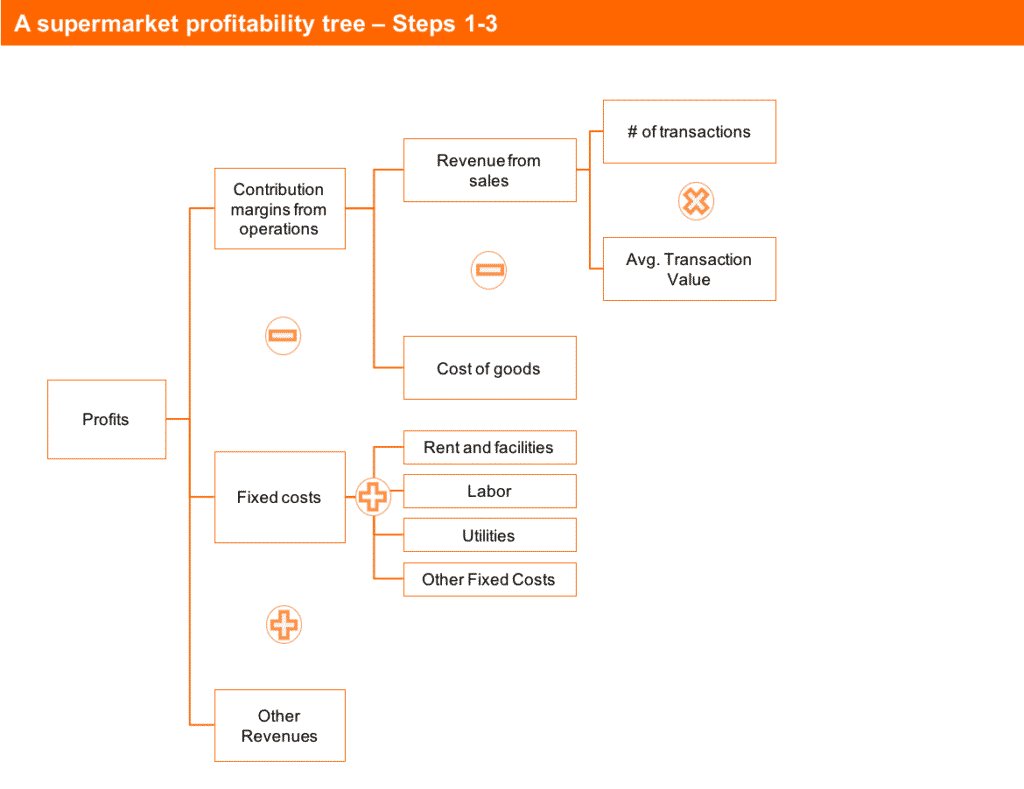

Now that we have a first layer and a specific cost structure for the business, we need to dig deeper into costs.

What most people do within costs is to break them down into Fixed and Variable costs.

And that works!

For starters, it’s an easy way to break it down.

Also, there are usually meaningful analyses that can come up out of it because these two costs behave very differently as the business grows.

Finally, it usually helps you think of specific cost lines for that specific business.

However, you could also use a “Direct + Indirect” cost structure, or even a Value Chain based cost structure, where each category is related to one step in the value chain (so, for an auto manufacturer that would be “Purchasing, Manufacturing, Quality Control, Sales + Indirect”).

These structures work. I personally use all of them, depending on the specific case.

However, you can’t stop there. You need to go deeper.

If you present a structure such as “Fixed + Variable costs” in a case interview, 9 out 10 interviewers will ask you this question:

“What are the main fixed and variable costs for a company like this?”.

This is a Brainstorming question, they want to test your understanding of business.

Why?

Because if they put you into a project in an airlines company and you can’t figure out on your own, before reading any reports that fuel and maintenance are two big cost lines in this business, you’re gonna be a pretty lousy consultant.

Notice that this doesn’t mean you have to spend late evening cramming what are the major costs in 20 different industries.

You don’t have to have read about business at all to infer that fuel and maintenance are important in the airline industry. All you have to do is to think of your own car and apply some common sense.

Or, you can use this method to think of your structures:

1) Put your “Fixed + Variable” structure on paper.

2) Hold a structure on the costs to “Make, Sell and Support” in the back of your head.

3) Think of cost ideas in each “quadrant” of your structure, as you visualize how that business makes and sell products (or services) and who is needed to support the operation.

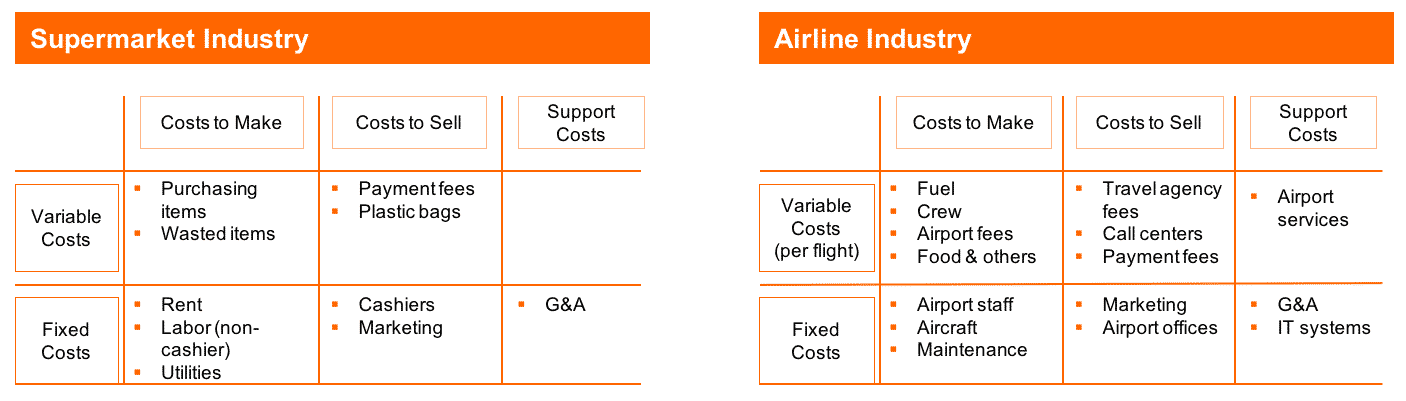

Here’s how this cost brainstorming technique looks like for the supermarket and the airline industries:

While you can show both structures used to generate costs to your interviewer, in most cases I’d just recommend showing the “Fixed + Variable” cost structure while keeping the “Make, Sell, Support” structure in the back of your head.

That helps to make things less confusing.

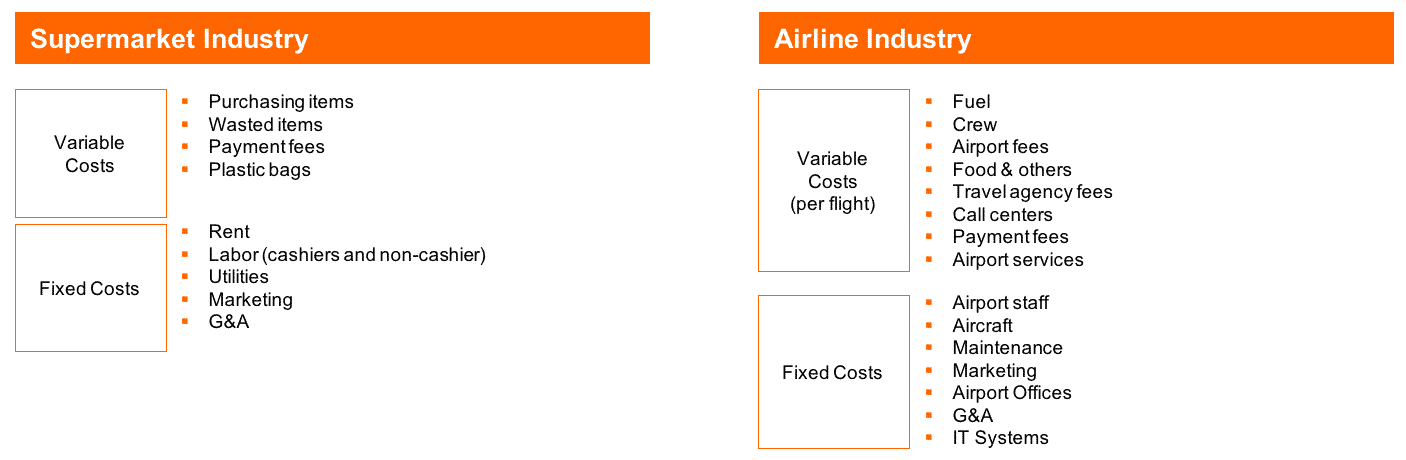

In practice, what you’d show to the interviewer is this:

When you use this technique, you know you have all the important costs of that business.

Why?

Because by using two structures in a “matrix” format, you’ve used a very granular approach to think of them.

You can explicitly show this secondary structure to the interviewer or not, but the important point is that you show your interviewer many of the specific costs that are important for that business.

Even better: explicitly tell them which ones are most important.

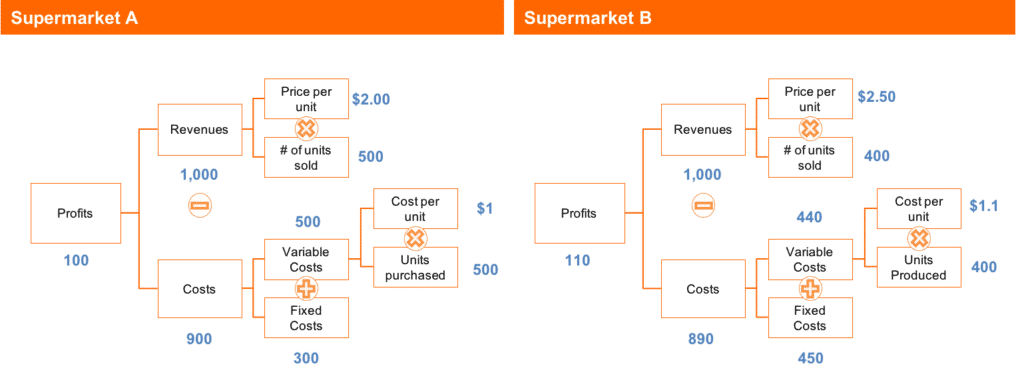

Clearly, in a Supermarket Business, purchasing items is very relevant.

Clearly, plastic bags won’t make or break a business in this industry.

But how about waste?

How important is that?

My guess is that it’s a bit important, but it’s more of an operational problem (having good inventory control, reliable refrigeration, etc) than a critical part of a supermarket’s strategy.

In a case interview, I’d make all this reasoning behind the importance of each cost explicit, as it shows thoughtfulness and it shows you know what you know and what you don’t know.

But Bruno, how do I know which costs are Fixed and which are Variable?

This is a question I get all the time.

People are told they should break down costs into “Fixed vs. Variable” and then they freak out.

They get insecure because they don’t know about a specific cost line.

They start discussing specific technicalities in an unusually nervous way as if they were about to anger the Cost Gods.

Let me clarify this for you, starting from the first principles.

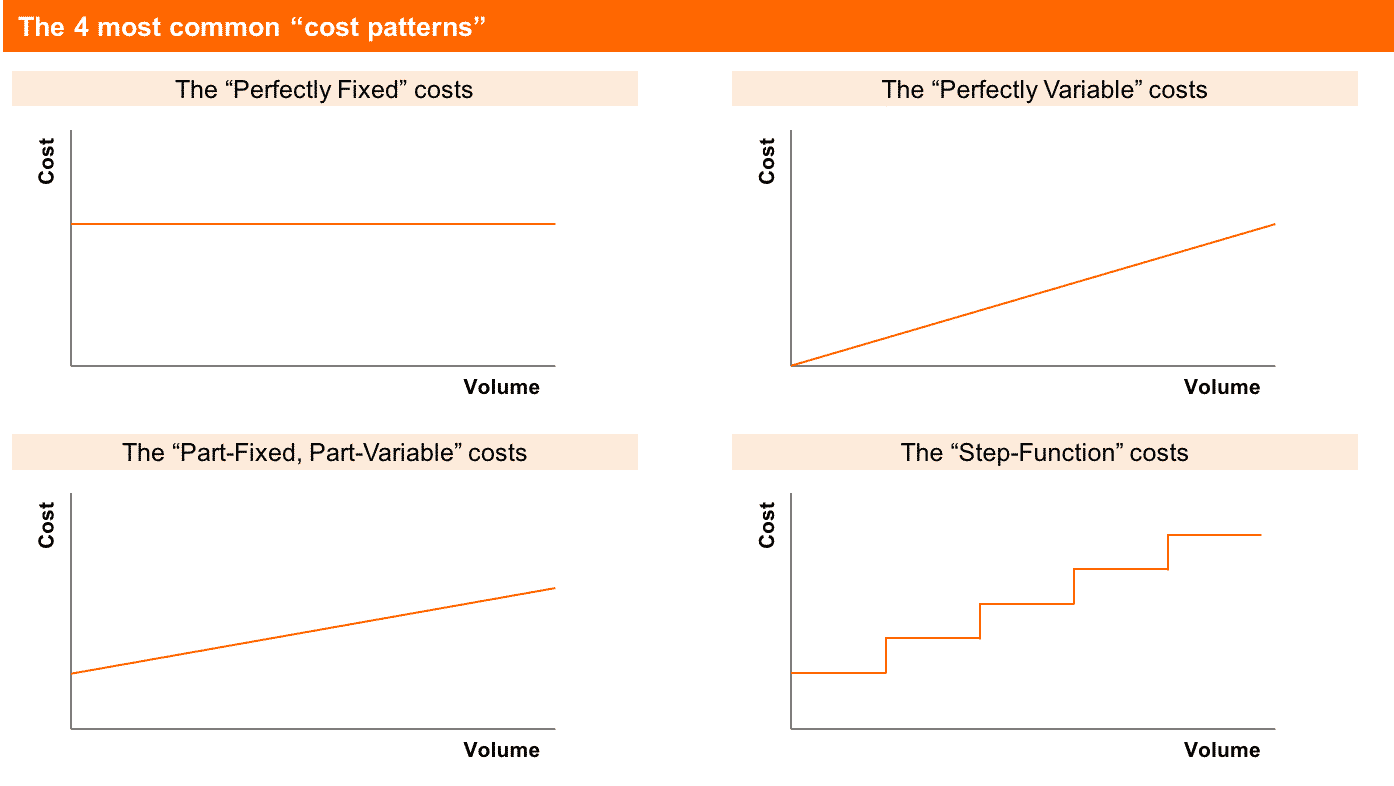

Why do consultants LOVE to break down costs into Fixed and Variable?

Because they behave differently.

Fixed costs stay fixed. (Or do they?)

Variable costs, well they vary.

But here’s the deal: while there ARE perfectly fixed and perfectly variable costs, most costs are in the grey area. And these generate the bulk of the confusion.

Here’s a useful guideline: if you’re unsure if a cost is fixed or variable, and you notice that “it depends”, categorize it where you think it makes the most sense and explain its behavior to the interviewer.

Showing you understand a cost’s behavior is more important than categorizing it in the “right” bucket.

Let me show you the 4 most common cost patterns that are common in case interviews and business problems in general:

Most of the confusion in the “is this a Fixed or Variable cost?” insecurity candidates have is NOT in the “Perfect Fixed” and “Perfect Variable” costs.

Most of the confusion in the “is this a Fixed or Variable cost?” insecurity candidates have is NOT in the “Perfect Fixed” and “Perfect Variable” costs.

No one thinks the products supermarkets purchase could be a Fixed Cost.

And no one thinks their G&A could be Variable.

What gets people confused is the 2 types of “grey area” costs.

Take refrigeration in a supermarket, for example…

Is it Fixed or Variable?

In my Supermarket Profit Tree, I have categorized it as a Fixed Cost (it’s implicit under “Utilities”). The reasoning is that even if a supermarket sells nothing, they’ll still have to pay for their freezers and electricity to keep them on.

However, one could argue that the more they sell, the more they’ll spend on refrigeration, so it should be a Variable Cost.

Who’s right?

Both! Refrigeration costs are “Part-Fixed, Part-Variable”.

So where should you categorize it? There are a couple of ways to think about it:

- You could categorize it in the bucket that represents the highest part – of a $1000 dollars spent in refrigeration, how much is fixed and how much is variable? You can put the cost in the part that represents most of the cost. But how would you know this if you haven’t worked in a freezer manufacturer before? You won’t.

- You could put it in both parts of the structure, and call one cost “Fixed Refrigeration Costs”, and the other “Variable Refrigeration Costs”. But should you spend that much time and energy in these minutiae? Probably not worth it.

So, what’s my recommended approach?

Put in the one you think makes the most sense and either explain to the interviewer that you’re aware that is partly fixed, partly variable OR don’t explain anything at all but be able to address that concern if your interviewer raises it.

Another thing that causes confusion in categorizing costs is that costs might vary according to many things.

For example, in the Airline Costs example, I’ve determined that what I call “Variable Costs” are “Variable Costs Per Flight”, not “Variable Costs Per Passenger”.

From a Passenger perspective, a Variable Cost per flight (such as the Airport Landing Fee) might as well be a Fixed Cost.

From a Flight perspective, a Variable Cost per route (such as the Regulator Licensing Fee) might as well be a Fixed Cost.

So before you call a cost Fixed or Variable, you need to explicitly determine what metric is it variable against.

(Or just be ok with the ambiguity, that is fine too).

Bottom line: Focus on being able to understand and describe the behavior of the cost, not the “knowledge” of whether it is “Fixed or Variable”.

You’re being tested for being able to realize the nuances and explain cost behaviors, not for “having knowledge” and “being right”.

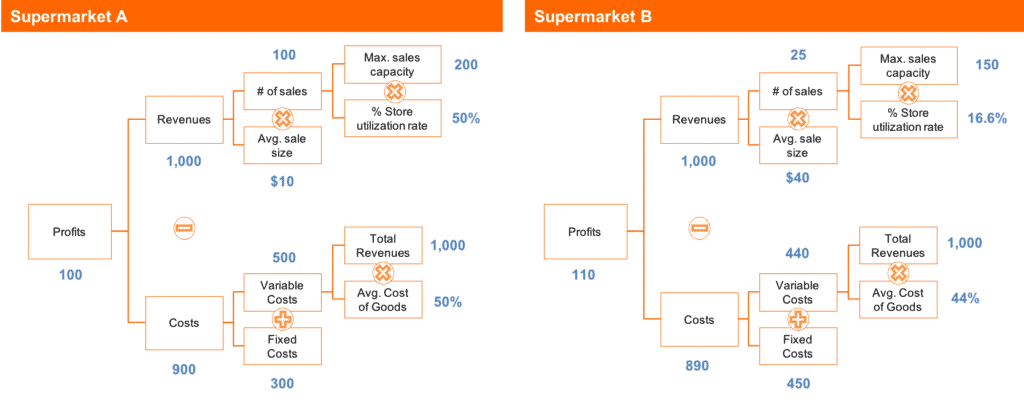

We could stop in Step #3 and have a profitability tree better than most.

If we built one for a Supermarket company up to Step #3, it would look something like this:

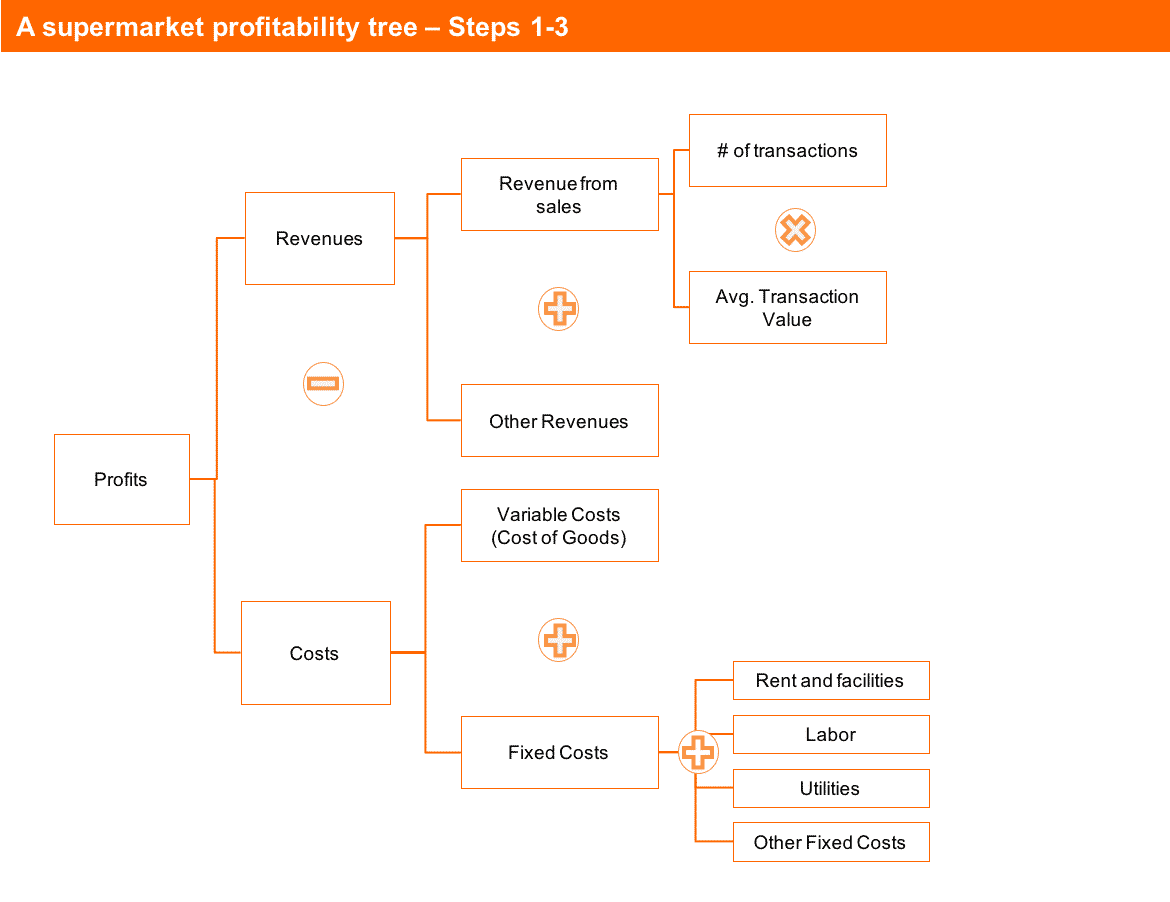

Or, even better – we can just keep things simple and use “Revenues – Costs” as a first layer. We’d have this profitability tree then:

Both trees are the same, in practice – the only change is how they’re organized.

I’ll talk about this last tree that uses “Revenues – Costs” as a first layer from now on in the article for simplicity’s sake.

So, we could stop here and have a better tree than 90% of candidates.

It’s even a good profitability tree for an experienced practitioner.

Why?

Well, because with a few questions about each bucket, you can get a pretty clear picture of what’s happening to a supermarket’s profits. In fact, in a case interview, this is the point where I’d try to get some data (before even doing Step #4).

But remember our original supermarket’s profitability tree I used as an example earlier in this article? It was special for three main reasons:

- It had a great first layer that described how a supermarket makes profits (though Revenues – Costs works well here too)

- Revenues and Costs were broken down in a way that resembled how the business operates (we’re still doing well here)

- It went deep into the most important, specific cost revenue and cost drivers

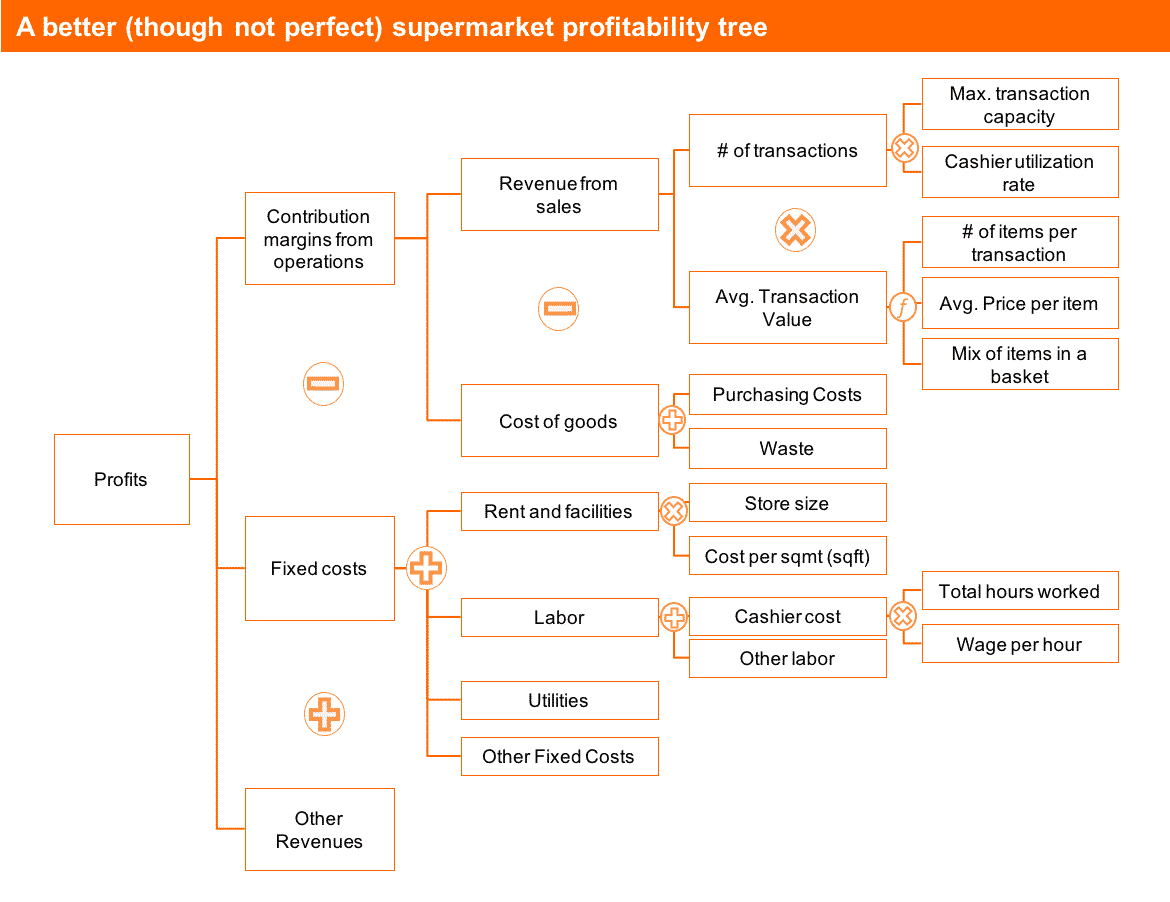

We haven’t covered this last point yet. An issue tree built with steps 1-3 simply cannot do this.

Yet.

So what should we do?

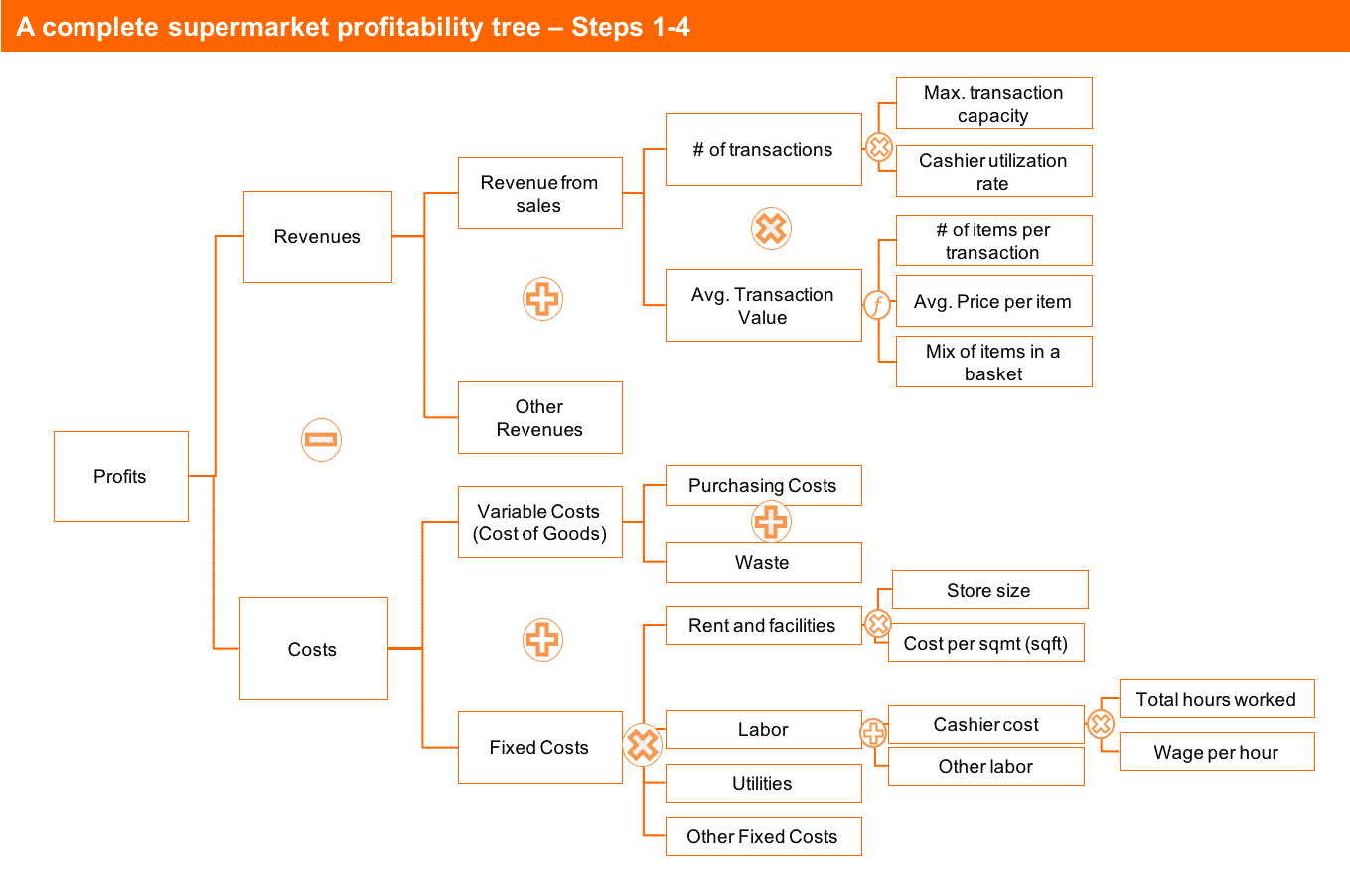

Well, we should pick the most important buckets from the profit tree we have and dig one level deeper. This is what will bring out the specific revenue and cost drivers of a supermarket.

- For “# of transactions”, we could look from the demand side (“# of total transactions in the region * market share”) or from the supply side (“max. transaction capacity * cashier utilization rate”). I’d pick the second as it’s easier to interpret the results of whether we should expand demand or cashier capacity in order to grow revenues.

- For “avg. transaction value”, the obvious way to break it down is “# of items per transaction * avg. price per item”, however, I’d like to bring the matter of which items are being purchased here too, so I’ll split the “avg. transaction value” as a function of those two things AND the mix of items in the basket.

- For the cost of goods, I’d break it down into “purchasing costs of items sold + waste of items not sold”. Some supermarkets may waste more than others.

- For rent and facilities, an obvious driver is the size of the store – if it’s too big, it will cost too much – so I’d break it down into “store size * cost per sqmt”.

- Finally, within labor costs, the amount of hours I’m paying for cashiers is extremely important especially if our “cashier utilization rate” is low, so I’ll create a structure that accommodates that driver.

Notice that I’m speaking about things very specific to supermarkets: cashiers, food waste, mix of items in the basket, store size and how many hours cashiers work in total. This specificity is what makes this step so important.

Here’s the final issue tree after adjusting for all the issues in the bullet points above…

(Besides the first layer, this tree identical to the one I’ve shown you in the beginning of this article):

This last layer gives our profit tree a specificity that makes it work ONLY in the supermarket industry.

It also helps us show the interviewer that we have a good idea of what are the important drivers in this type of business.

In a real-world analysis, this would help us use the tree to find all different types of KPIs for the performance of this store. Here are a few examples of metrics you could derive from this tree:

- “Cashier wage costs per transaction”

- “Cashier wage costs per dollar spent”

- “Revenue per sqmt (or sqft)”

- “Waste costs as a % of revenues”

And so on.

A tree like this is a great tool to diagnose profitability problems in a supermarket, and even to manage one!

Now, enough with supermarkets!

In the next section, we’ll see three examples of profitability trees we could build for other industries using this same technique, what makes them GREAT, and what types of insights we can derive from them.

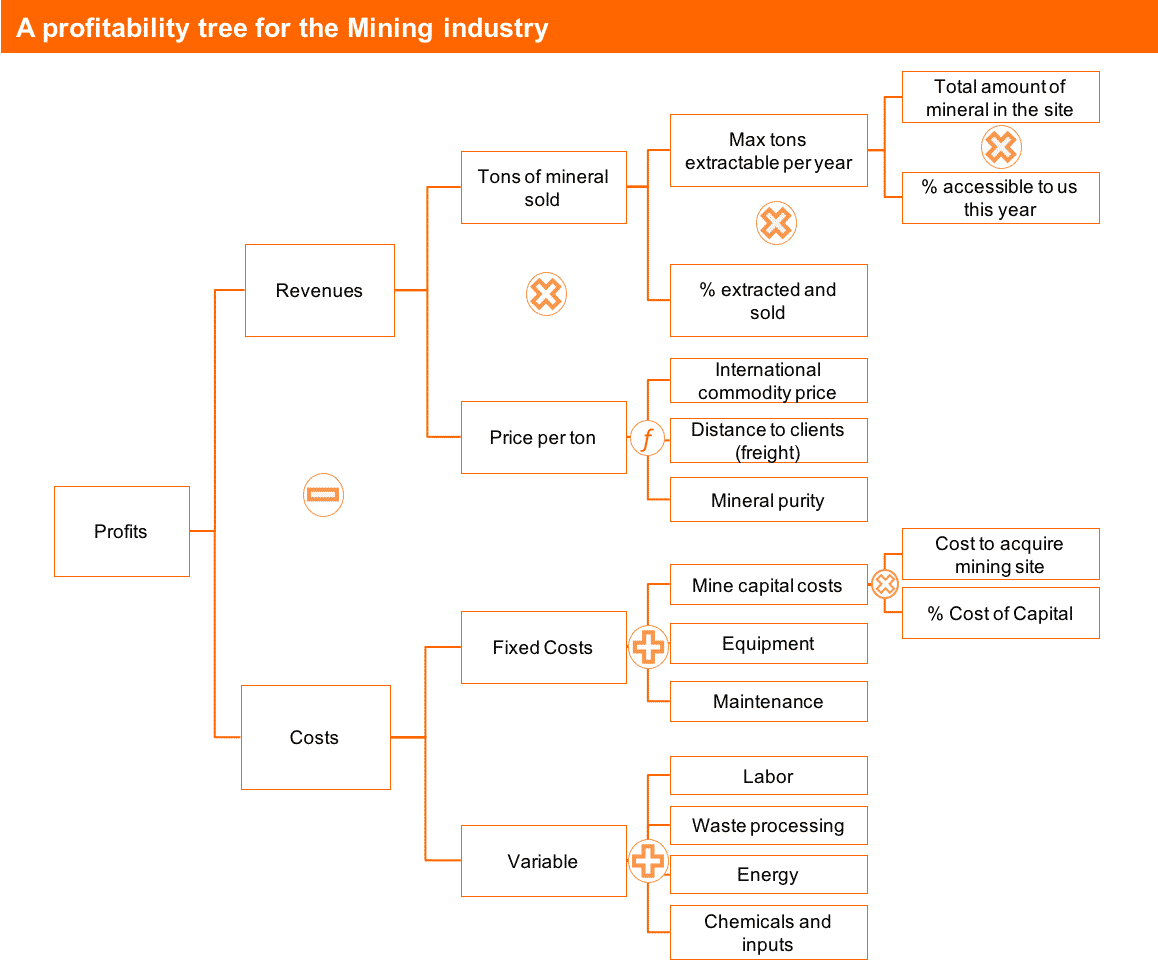

For this example, I’ll show you a profit tree for a mining company that has ONE mine that mines ONE mineral (think something like iron ore).

So, how did I build this tree?

First of all, I’d love you to know that I have NEVER worked in mining before and that I didn’t research the industry before building this tree.

Why?

Because I want to keep real with you. I want you to see how you can use this tool to build a good structure in your interviews.

In a real-life consulting project, I’d probably start off with a tree like this one (that I created using my own judgment) and then I’d research the industry and talk to people to improve it.

I’d validate buckets that I’m not sure should be here, and try to find new buckets that I haven’t thought of.

Now, let’s review how I built this tree following the 4 step approach I laid out earlier in this guide:

Step 1: Choosing the first layer

I just went with Revenues – Costs.

I did it because it works and there’s no need to overthink this.

Seriously, it’s that simple.

(To be honest, I also thought I’d include revenue from “extra” minerals we could find while extracting the main mineable mineral in this mine. I decided not to include it to make things simple, but this is one thing I’d keep in my head and if there were any indication during the case that it could be an issue, I’d look more into that).

Step 2: Choosing the Revenue Model

This is one industry where “Price * Quantity” works well enough, so I just used that.

Within “Quantity”, however, I followed an approach that is unusual to other industries.

In most industries, how much you sell depends more on how much you can get other people to buy from you that in how much you can produce. You’ll usually break down total volume sold as “Total Market Size * Market Share”, or something similar.

In the mining industry however, because most minerals are commodities (and I’m assuming this one is), you can sell roughly as much as you can produce, as long as you’re producing it below market prices.

In reality it’s not this simple, but still… Most mines are able to sell as much as they produce (as long as there is one other mine that has higher costs than they do).

That means I chose to break down “Tons of mineral sold” as “Max tons extractable (which is the maximum capacity)” * “% that is actually extracted and sold”.

Now we have a customized revenue model for this mining operation. I only included the details later, on Step 4, so let’s jump into the cost structure.

Step 3: Creating a cost structure and listing major costs

Here I just used the “Fixed + Variable” mini-framework.

It makes sense and it helps solve the problem.

One question that went through my head (and that should always go through yours) is: “variable to what?”.

I defined “variable costs” as costs that vary according to “tons of mineral mined”, that is, quantity. It’s pretty obvious, but it’s also an important mental step to go through so your structure makes sense in the end.

The next thing to be concerned about is to list of all of the major costs.

Earlier in the article, I mentioned you can have a secondary, “back-in-your-head” structure of costs to “make, sell and support the operation”.

This would NOT work well here, because in a capital-intensive, commodity business such as mining, the costs to sell (and even support) are negligible.

HOWEVER, we can still use the same principles to help us out here.

The principle behind the “make, sell, support” mini-frameworks is that these are the broad processes underlying the work of any company.

In a mining company, the broad processes that underlie it are:

(1) Setting up the mine and equipment to it’s mineable,

(2) digging, mining and separating the soil/rock,

(3) moving stuff around (metal and dirt) before you can sell it.

This is the “mini-framework” I kept in the back of my head while looking for fixed and variable costs.

And because of this “mini-framework”, I was able to find costs that are highly relevant for the mining industry that most candidates would not notice, such as “chemicals and inputs” to separate metal from soil, “energy” to power the equipment and vehicles, and “waste processing” because you have to do something with the mountain of material you’ve moved around (along with all the chemicals that you used).

Step 4: Going deep into specific revenue and cost drivers

I chose 3 main drivers of this business to dig a little deeper.

Here they are:

- “Max tons extractable per year”

- “Price per ton”

- “Mine capital costs”

I chose these drivers because (1) they’re HIGHLY relevant to how profitable a mine is, and (2) I don’t think just looking at the number would paint a detailed enough story.

For example, when I looked at “Max tons extractable per year”, I immediately thought that if this number were low, I’d be in doubt if this was a problem with the mine site (how much mineral was in there) or with how much we’ve developed it (how much of that mineral is currently accessible to us).

These are two completely different problems with completely different solutions.

And when I looked at “Price per ton”, I thought there was more to it than the number you see in the Bloomberg terminal or when reading the Wall Street Journal.

Maybe customers are willing to pay more for our mineral because it’s purer. Or maybe they’re willing to pay less because our mine is so far away, and metal is so expensive to transport, that unless we charge less, they’d rather purchase mineral from a more local supplier.

And when I took a look at the cost of the mine itself, I immediately thought: “if we’re spending too much on it, is it because we overpaid for the mine or because our financing conditions sucked?”.

Going into depth in drivers I deem important in an exceptional way to show two things to the interviewer: (1) you can go into depth if needed and (2) your structure is uniquely created by you.

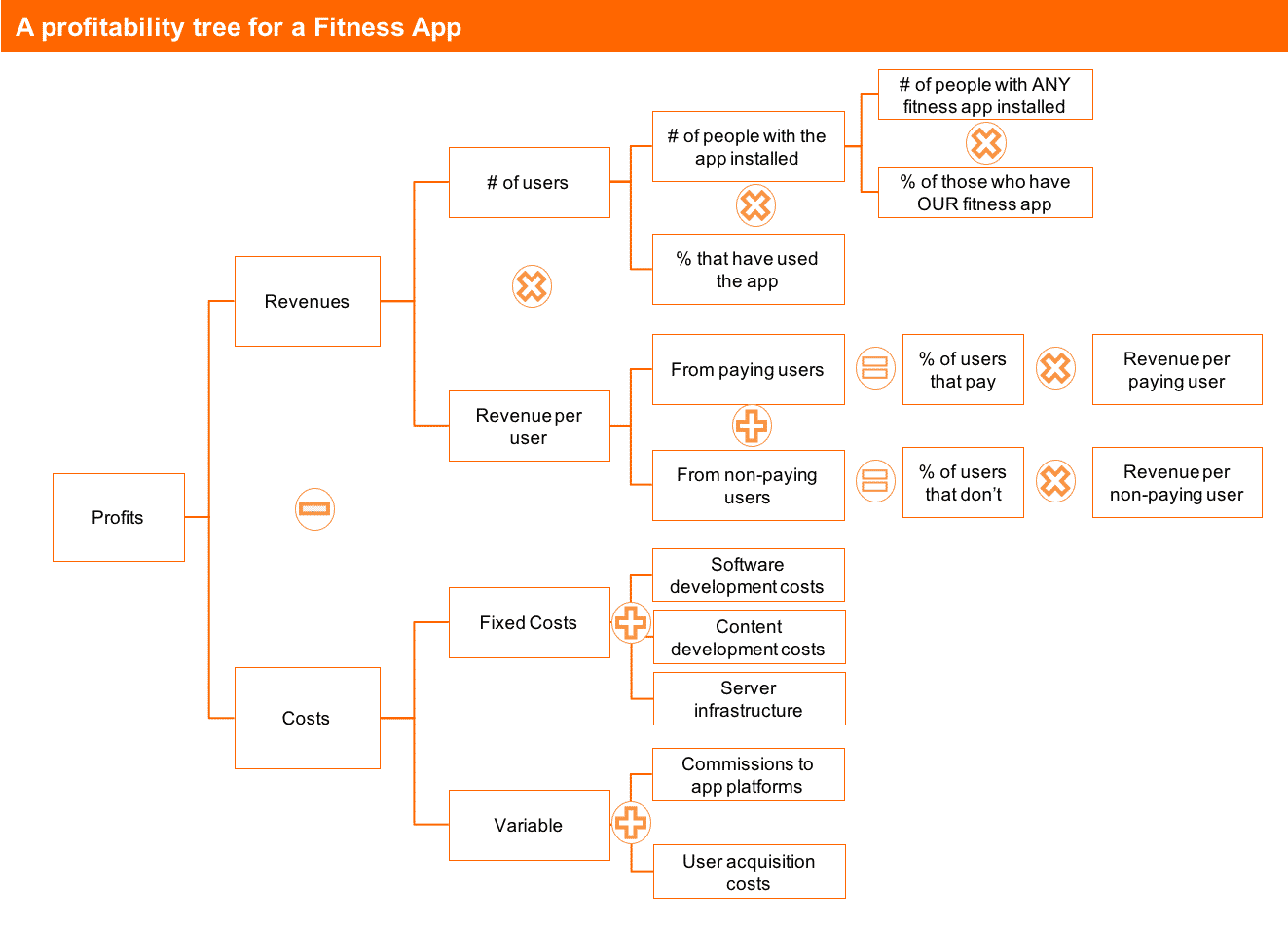

What’s the opposite of mining?

I don’t think this is a valid question, but if it were, I’d say a Fitness App is a more than acceptable answer.

So, let’s exercise our Profitability Tree muscles (pun intended 😉 ) and build a profit tree for a company that makes and distributes a smartphone fitness app for Android and iOS.

Here it is:

I won’t go into as much detail on how I built this as I did in the Mining example as I think you’re getting the idea of how to build it already. So I’ll skip into the highlights and key points:

I won’t go into as much detail on how I built this as I did in the Mining example as I think you’re getting the idea of how to build it already. So I’ll skip into the highlights and key points:

- For the Revenue model, I have used a “# of users * Revenue per user” structure. It makes much more sense than “Quantity * Price” (quantity of what? Couldn’t it be a subscription-based app?) and describes beautifully the main growth driver of an app is to have more active users.

- I have considered that a Fitness App can get revenues from paying AND non-paying users. They can, for example, have advertising revenue from the non-paying folks if they operate on a freemium model (as most of these apps do). This is an important insight to have as you build the tree.

- I have considered that most people choose that they will download a fitness app first and THEN decide which one. (Hence the “# of people with ANY fitness app * % of those who have OURS” formula). I have also considered that not everyone who downloads it becomes an active user (which is essential to generate revenues).

- On the cost side, the most important insights I brought are: (1) there is not only software development costs, but also content development costs (e.g. videos of the workouts), (2) you may have to pay commissions to Apple/Google for the revenues you generate from their apps, and (3) if you have a predictable marketing funnel, user acquisition costs (i.e. spend on ads, if that’s your marketing channel) are variable relative to the number of new users on the platform – the more you spend in ads, the more users you have.

Not to say that this profit tree is perfect (it isn’t), but your goal is to bring as many insights about the business model embedded in the structure as I aimed to do in this example.

It is hard to think how this profitability tree could be used outside of the smartphone app industry, and it’s hard (although possible) to think about things that are highly relevant to this industry that I haven’t mentioned in this tree.

These two attributes from the last phrase are what makes it an excellent profit tree to work with.

One thing I want you to notice: I have made a bunch of assumptions regarding the business model of this Fitness App that may or may not be valid (as different fitness apps have different business models).

Among them:

- That they are on a freemium model (or that they could turn into a freemium app if they wanted)

- That they produce their own content (most fitness apps do, but some, such as running trackers, don’t)

- That they acquire users through advertising (again, most apps do, but some don’t have variable user acquisition costs)

It’s okay to make these assumptions as long as you make them explicit in an interview. Even better: ask the interviewer if these assumptions are true as you build your tree.

They’re gonna be glad you did that.

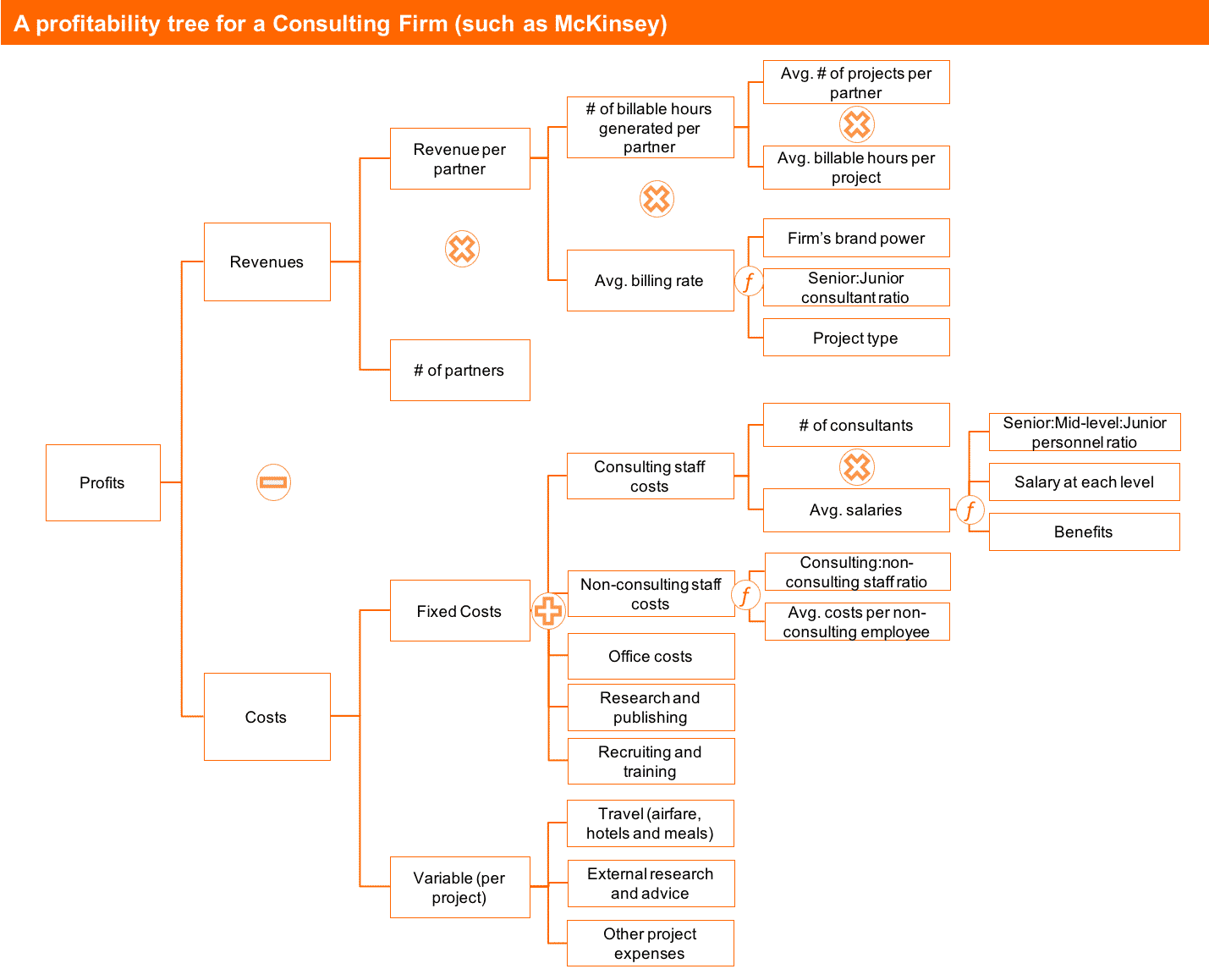

I’m taking some risk doing this one.

I’ve worked at McKinsey and am now teaching you how to use one of their main tools to analyze McKinsey’s own business!

You probably expect I pull off a damn good profit tree here.

I’ll do my best, I promise.

Anyway, my goal with this last example is twofold:

(1) To help you solidify your understanding of how to build profitability trees for any industry,

(2) To help you understand a bit more about the consulting business model (always good to know about that).

But for this example, I want YOU to follow the 4 steps and build a profitability tree for McKinsey or BCG or Bain as if you were running the business before you compare it to mine.

Go grab a piece of paper (and maybe brew a good cup of tea or coffee) and do it before you reveal my tree.

I promise you it’s gonna be worth it!

Once you finish building your own, take a look at mine here:

It’s not a perfect tree. No tree is “perfect”… But one can draw insights from it.

It’s not a perfect tree. No tree is “perfect”… But one can draw insights from it.

Here are a few of them:

- I chose to structure revenues with Partners as the drivers. As anyone who’s watched the TV show Suits, you know partners are the people who bring in clients to professional services firms. So a firm can grow by having more revenue generating partners or by having each partner bring in more revenue (the second option is preferred). There are many ways partners can do that, as you can see on the tree.

- I could’ve structured revenues differently. That’s true for any industry, but especially so for consulting. There are many ways I could’ve done that. A firm with very loyal clients could choose to see their revenues as “revenue per client * number of clients”. A firm with a sales process that doesn’t depend on partners could see it as the “# of projects * revenue per project”. It all depends on the specifics of the situation.

- The consulting business model is all about balancing “Revenue per Partner”, “Leveraging” and “Staff Costs”. As I said earlier, a good Profit Tree lets you take a sneak peek into an industry’s key business drivers. In the case of consulting, it’s all about balancing three things: (1) how much revenue a partner brings in, (2) how much work a partner “leverages” with more junior consulting staff and non-consulting staff and (3) how much that “leverageable” staff costs. Obviously, other costs and how many partners are there in a firm matter as well, but these are afterthoughts compared to the first three things. The Profit Tree helps you see that (although you definitely need to have a critical eye when you look at it).

- Staff costs are fixed on a per project “view”. Top consulting firms rarely hire because they’re getting a couple of new projects in the office. And they rarely fire based on a shortage of engagements. That means their main costs are fixed against revenues (in the short term at least). This explains, in part, why the industry is so competitive and hours are so long: they’ve got to pay the bills, so they’ll work as hard as possible to keep their clients and generate new projects.

How does that compare with the tree that you drew? Can you take the same insights out or your own tree?

Let me know in the comment section at the bottom of this article!